But first, some thoughts on the current business environment…

For those of you who follow me closely, you will note I have not written a blog in a long time. When Covid hit, it just did not seem to be the time to promote ideas about recruiting, hiring, and all things business that I cover in my blogs. What has been shocking to me is the pace of business…it has not slowed down at all for the tech companies we at Arnold Partners supports. Honestly, this has led to some degree of thriver guilt – to see so many fellow citizens (and in many cases very good friends) struggle in this K-shaped economy we are living in. In the direct world where I focus, the demand for CFO talent has never been greater. Tech IPOs are booming, which has a direct effect on the overall CFO market. As CFOs get drafted up into IPO companies, it frequently leaves a void somewhere down the food chain of the tech continuum. This has certainly had a welcome effect on our business and frankly has kept me from taking time to blog about this or that or the other thing. But now, following a brief respite, on with the show!

Continuous learning…

It is something we all muse about in both our personal and professional lives. Some of us actually try to do a bit of it…I still take a saxophone lesson every week, even if my skills seemed to have leveled off. I was taking Spanish classes when Covid hit, but those are on hold. It is especially important for me to always be learning. Whether a new skill or tactic, or perhaps even a whole new strategy around hiring.

I had an “Aha!” moment last year as I took on a fairly early-stage client needing a CFO. One of the clear mantras of the culture in the company was around continuous learning. Everyone in the company is encouraged and engaged in learning something new all the time. It could be how to juggle or how to improve listening skills. It does not matter as long as it is something outside of work that involves learning. When I met the CEO, I knew we were simpatico on that and immediately wanted to support him in finding an excellent CFO. (Which we did, and all went well!)

Learning a whole new approach to interviewing candidates…

The prospect of a taking a new tack for interviewing candidates was an entirely different kind of challenge. I mean, come on, I have been interviewing finance pros since 1992. I think I know what I am doing! Along came another client who had a VERY specific approach to the hiring process based on a book written in 2008. When they informed me of their dedication to this technique, I quickly got the book and read it from cover to cover. Three times. I went back with a highlighter to study certain elements of the process outlined. It was exciting. Some new ideas, some GREAT ideas and as it turns out, some really interesting learnings in the actual process with CFOs. Not as expected!

First, the positives:

The book gives a particularly good template to design a job spec that actually fits what it is you want to hire for. This may sound obvious, but I will tell you from experience, most companies take a spec off the shelf and maybe customize a line or two for their needs. By really thinking about what problems, you are trying to solve at the beginning of the process, it definitely makes screening candidates against a specific wish list of skills and experience for the exact needs of the client more effective. I have written about this before in a blog, “For CEOs and CFO Candidates: The Importance of an Exacting “Spec” in Executive Recruiting,” and the authors got it right.

The real aha in the book for me was around having various members of the interview team focus on different areas of expertise and skills of the candidates during the interview process. So often after a series of interviews candidates will tell me that everyone asked them the same thing. Or that they spent the first 10 minutes of the interview talking about something completely off subject such as a hobby. If there are six people on the interview team and each one spends 10 minutes talking about the same hobby, your interview team just spent a whole hour on it – not exactly productive! The takeaway is to have people on the team with specific skills or knowledge to hone in on those areas you are seeking in the candidate. Certainly, overall impressions are still made with each interview regarding communication skills, reasoning skills, presentation, listening, etc. So even tho each interviewer had a specific task, each contributes to the overall assessment.

The authors also offer a great litmus test to getting to a “no” on a particular candidate very quickly. Focusing on what the candidate’s recent former bosses say about them early on in the first call reveals whether or not their bosses have confidence in the candidate and will stand up for him/her.

Now the negatives:

The overall arch of the first five or six meetings as outlined in the book is heavily weighted to the company who is evaluating the candidate and offers very little opportunity for the candidate to ask any questions about the company, the role, or even the people they are meeting. In practice, this was a particular turn-off to CFOs. CFOs are data driven. They want to learn about and be sold on the opportunity as much as they like to show off their abilities to ask penetrating questions. We lost some good candidates that were totally turned off by this one-way approach. I think it may have something to do with the book being written in 2008. It was a buyers’ market for talent in 2007-2009. Not anymore. Not by a long shot. (Credit – when I gave the client this feedback, we altered the process a bit to give candidates an early opportunity to learn more about the company.)

Specific to my client, the first “real” interviews between the company and the CFO candidates after passing a 30-minute screen with the CEO were conducted by a very junior person on the staff. While this staff member is really well respected within the organization, the feedback from CFOs was basically they felt insulted and a real reluctance to continue the process no matter the outcome of the meeting. CFOs were telling me that spending an hour being grilled by a person with three years’ experience out of college sent a message that the company did not know what it was doing. (Credit – after a few of these meetings, the client heard the feedback and altered the process). I have another blog to follow this one about hiring a CFO and how much weight needs to be from “the team” (code for the people who would report to the CFO), the “executives,” and the CEO/Board. Stay tuned…

Conclusion on the book:

It was well intended. As with most business books there were a few good nuggets. I did take away some good learnings, both positive and negative. But to apply it literally to each hire was misplaced. CFO hires are unique. This hiring template was unique but the two were not really compatible. Fortunately, my client was open to feedback and we were able to alter the process and ended up making a great hire. If you want more details, please reach out…good to be back. More soon, Dave.

Without exception, my conversations with executives all begin or end with, “What strange times we are living in at the moment,” or something similar. No one seems to be able to make sense of the big picture right now. From what I have read, it is because we are not conditioned to understand events that have no clear timeline to conclusion. Almost all endeavors we embark on as humans have a delineated end — this pandemic does not. We are cautiously “opening” up while new cases of the virus continue to accelerate in many states, including California. With all of this as a backdrop, it is on the surface hard to think about hiring a new CFO or VP Finance for your company. But this is the exact time you need to think contrary to the pack. Here is why.

Shelter in place creates a unique recruiting opportunity

Since early March we have seen a marked increase in the number of “confidential” searches coming into Arnold Partners. Smart companies are taking advantage of the ability to meet candidates virtually and in complete confidence during this unique moment in time. It works well for the confidential passive candidates most companies want to hire as well. They are in a great position to take meetings without the necessary excuses of where they are going or why they are not in the office. The best recruiters know and target passive candidates, and in this work from home environment, the ability to grab the attention of this passive population is uniquely available right now. The last VP Finance search we completed in 30 days because we know who to tap.

But with a recession going on and companies laying off 1000s?

The focus at Arnold Partners is technology companies of all stripes. This sector has certainly seen a number of verticals hit in the downturn — travel and some med tech companies come to mind. Early stage tech companies without ample funding may not be in the market to add executive talent either. But if you are the CEO or Board Member of a well-funded tech company, now is the time to take inventory of your C-suite and VP-level talent and decide if it is time for an upgrade. How has your CFO done throughout this pandemic? Was the company well-prepared from a cash standpoint? Was the CFO able to tap banking relationships to shore up the balance sheet?

The best time to upgrade is at the start of a recession when executives from other companies may be concerned about the future of their career in-place. Now is the time to pluck from your competitors or near competitors to strengthen your team. But you need the right help.

Partnering with the right search firm and consultant

The best search consultants will truly consult with you and your team to determine how to improve the mix of both talent and diversity in your executive ranks. Search consultants do not just “take job orders.” They help craft the specification by carefully listening to you and by gaining an in-depth understanding of the business you are in and what the road map to success looks like. But then, only the best of the best consultants can reach into the vast pool of talent to pluck out a select list of passive candidates, who will not only take the call from the consultant, but also take the meeting with the prospective new employer. This process is part science, part art, and usually a culmination of many years of hard work, and it is certainly the way Arnold Partners continues to deliver. View my video for a list of questions you may want to use when interviewing an executive search firm:

Setting the right tone for a confidential search

This all may sound a bit cloak and dagger and nefarious — sneaking around your competitors’ home offices to steal their talent away! (Although that is the nature of recruiting.) But this is the key reason why it is so important to partner with the right search firm. The connected firm can quietly target the right people without resorting to any publication of your needs. Because of long-standing, curated relationships Arnold Partners maintains with the top finance professionals, the risk of word getting out that we are working on a confidential search is almost nil. When we make those calls into our network, we set the right tone during the very first call with each prospective candidate. The efforts to upgrade your team can be achieved quickly, quietly, and effectively. It is really important in a confidential search that your company and motivations will be represented in the most ethical and accurate manner by a trusted professional like Arnold Partners.

I invite you to contact me at moc.srentrapdlonra@divad if you would like to talk about your needs and explore upgrading your team. Stay safe and healthy, David Arnold President, Arnold Partners, LLC Strategic CFO and Board Recruitment

With your newly crafted executive resume in hand, it’s time to get to work on getting the right people to see it and invite you for an interview. Again, the goal of the resume is just that: to open doors to a conversation about new opportunities for you as a professional. But as we climb the latter into executive roles (VP and above), fewer and fewer positions avail themselves (as math dictates). In addition, many of these roles are not advertised in public forums.

Here is my advice on how to network yourself into a new role.

Moving on

For the sake of this article, let’s just assume that you have made up your mind to seek a new professional home. Maybe your commute stinks, your company has flatlined in growth, you have a new boss, or that side project you just completed really got you excited about using a different skill set. Whatever the reason, it is time for a change. Most professionals at this juncture reach out to the three or four executive recruiters they know to see what is happening. There is nothing wrong with this approach, but there are better ways to take charge of your search.

The brainstorm

The first step in this process is getting out a pen and paper (or a spreadsheet) and writing down a list of the most influential people you know. These are people who would return a call or email and who would be willing to make some time for you. But they are also people who are in a position to make introductions that matter. This list should include investors, board members, CEOs, professors, MBA classmates, peers in other companies you work or compete with, etc. These are folks who are in a position to introduce you to other people in charge of executive hiring.

Note: That list does not include executive recruiters. Think broadly while scribbling your list, and include some stretch goal people. Get at least 50 names down, and shoot for 100. Take a few days and retrace your career. Find lost contacts. LinkedIn is a great resource.

Top 10

Once you have your long list, study it, and rank the top 10 people on the list. Your goal now is to arrange one-on-one meetings with those 10 people. Your ranking should be a weighted combination of how influential the contact is and your ability to get a meeting with the person. Be realistic and just a bit idealistic. You want wins (getting a meeting), but you do not want to set yourself up for disappointment by aiming too high. This is a game and a sport, and if you approach it as such, it can be fun, stimulating and ultimately rewarding.

Getting the meeting

Narrowing your list to the top 10 makes the networking game more realistic for a working professional. These meetings are hard to get and hard to schedule since everyone is busy. You are asking for time on an executive calendar, so be realistic and persistent and respectful. If you can get two meetings a month, that would be a win. Three would be fantastic. In my experience, if you get 10 meetings in a few months, new opportunities will present themselves, either directly through these contacts or through their network. In a world full of noise, interruption and email bombardment, you need to be top of mind.

Being crystal clear

So what to do when you get the meeting? This is where the elevator pitch is key. You may only get a few minutes with these influential people, so it is really important to be clear about why you are there and what you have to offer. You should have your personal elevator pitch down to three or four sentences with an easily understood takeaway (e.g., how your skills and experience can help transform an organization). This elevator pitch should be repeated in the summary of your resume to reinforce your message. You should also be in a position to offer help to the executive you are meeting with, so be sure the conversation is a give and take.

Be respectful of this person’s time, and don’t go over the allotted schedule. Follow up with a thank-you email and an offer to be a resource for this person in their line of work. Reiterate your goals and skills. Be brief and to the point. Set a reminder to follow up with this person in 30 days via email.

In my experience, establishing a plan like this makes the likelihood of introductions to new opportunities very high. It takes work and dedication, thoughtfulness and persistence. But it works. As for the recruiters I left out of your “influential” people list, I mean no disrespect. But we are tasked with finding very specific people for our clients, and while we play an important role in building a career, don’t stop there.

The work I do finding exceptional CFO and Board Members for my tech and life sciences clients is not exactly steeped in numbers. It is more about communication and networking. Sure, there are metrics that I use to measure my business, but they are not nearly as important as the metrics that CFOs live by as they contribute to the companies where they work, e.g. increase in company value through driving innovation and efficiencies in all aspects of the business. But as we come to the close of 2019, it struck me that there are many important numbers that reflect the work of Arnold Partners and I’d like to share them here.

10

10 solid years Arnold Partners has been in business! Pretty cool. In that time, we have placed 70 CFOs for technology companies who have helped their companies increase in value by over $15B. I am probably undercounting that contribution because it only is a calculation of IPOs (Market Cap) and the M&A exits that have taken place with my placed CFOs. Of the 70 CFOs I have placed 11 lead IPOs and another 18 lead M&A exits. Pretty sure the other 41 have increased the value of their companies through further fund raising or just top line growth but it is more difficult to measure. What does all of this mean? For one, the focus of placing CFOs for me is on creating value—for the enterprise that hires me, for the CEO I so closely work with, for the investors behind the enterprise, and for the CFOs themselves. 10 years also means that we have made a name for ourselves in the technology marketplace as a leading resource for top CFO talent. I am confident we will be repeating this blog on our 15th and 20th anniversaries.

96.5%

That is our completion rate for the searches we have taken on in the last ten years. Why is that important? The retained search industry reports from publicly traded firms indicate their completion rate ranges from 70 to 80%. No one is in the 90% range, let alone almost 97%. This means that we complete our commitments to our clients. The large search firms charge 100% of their fees but only fill 75% of their engagements. Not here. We are in it to win it AND finish it for our clients. A related number is the “stick-rate” of our placements. Just finishing is not enough, we want to make sure the CFO we place is still on the job 1, 2, 3 years after accepting the role. And they are. Of our 70 placements, only in one case did the CFO not last. So that is a 99% stick rate.

9

Is it simply the economy or are we getting better? Or word of success getting around? We completed 9 CFO searches this year up from an average of 7 in years past. Our time from inception of search to completion is also improving, from 115 days in 2018 to 103 days in 2019. I suppose if the economy tanks the demand may not be as robust for search services, but we lived through big downturns before. We are going into the new year with an active search and one more agreed to kick off in January, so maybe 2010 will bring us to 10 completed searches!

30

On a personal note, I celebrated my 30th wedding anniversary with my wife this year. If you want to put a strain on your marriage, triple your mortgage and then tell your spouse you want to start your own business! The truth is I could not have done this without her. She is the silent partner in Arnold Partners. Well, not silent with me. She kicks my butt and keeps me going and keeps me measuring the business. If we are not getting better and faster and keeping clients happy she will let me know about it. I am blessed to have her unyielding support. She is my CFO!

3,371

That is how many people this blog is being sent to via LinkedIn. Thank you all for your support over these last few years. I could not make my world turn without all of you! I wish you all a very happy Holiday season and an exceptional 2020!

If you are looking for exception CFO or Board Members in 2020, please shoot me an email at moc.srentrapdlonra@evad.

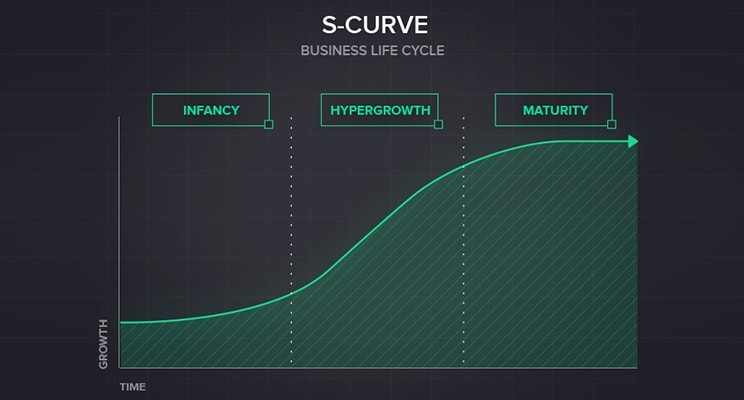

CFOs play a vital role in the scaling of any business. Young technology businesses however pose their own unique challenges. Coupling those challenges with hypergrowth results in extraordinary demands on the management of a company. First coined by Alexander V. Izosimov in the Harvard Business Review in 2008 Managing Hypergrowth, “hypergrowth” refers to the steep part of the S-curve, where industries and firms grow at an explosive pace. Hypergrowth businesses rapidly expand with compound annual growth rates (CAGR) that can exceed 50%, and in some cases even above 100%. This means hypergrowth companies need to insure they have the right people and systems in place to support such high velocity, so they do not go off the rails.

At the same time, the CFO role has extended its reach into every corner of a company. In most companies the CFO, more than any other executive, is a true business partner to the CEO. Therefore, as hypergrowth companies work at a frenetic pace to meet the many challenges, chances are the CFO will play a major role. So how can CFOs effectively expand their influence and add value in these hypergrowth technology focused environments?

Think Strategically

In many companies, CFOs are being called on to play a bigger role in setting strategy. The CFO’s traditional role as steward, operator and catalyst now includes a large dose of strategy in addition to the more traditional role that focuses on core competencies such as accounting, tax, financial reporting, internal controls, budgeting and forecasting, investor relations, fraud awareness and prevention, risk management and corporate governance. This was certainly the case in some of my previous roles as CFO where I was responsible for the Strategic Planning function. In order to expand their skill set, CFOs must therefore move up the value chain from being stewards of compliance to becoming strategic executives.

Developing a strategic view requires gaining a holistic understanding of a business and starts with understanding the product value proposition.

Why are customers buying the company’s products?

Does the company have a repeatable solution that is solving a clear pain point?

Are the unit economics self-evident, sustainable, and based on relevant metrics?

Where is the company in the product adoption lifecycle?

How does the company aggressively extend its product relevance to rapidly gain share?

How can strategic M&A further accelerate share penetration by filling in product gaps?

The most effective CFOs can serve up cogent, actionable answers to these critical questions. While this does not mean the CFO needs to be an engineer or a technology guru, it does mean the CFO should understand what is driving top line revenue, the core of any hypergrowth business. Even if there is a separate strategy function reporting into the CEO, which is not uncommon, the CFO should engage with the strategy team and understand the competitive dynamics and clear choice the company has made to either disrupt an industry with entrenched incumbents or pioneer a new market. Developing this understanding is crucial for finance leadership to play an active role in making decisions on capital allocation.

This includes a more detailed roadmap for the specific areas where the company plans to innovate and the related cost drivers. For example, with software businesses, understanding the extent of “Tech Debt” may sound at first like it is beyond the scope of finance leaders. Tech Debt is cholesterol in the arteries of startup growth: the overhead associated with previous shortcuts being taken in software development which increasingly impede future scalability efforts. This is important for the CFO to consider because it directly impacts future costs which need to be accounted for in the financial model to allow a company’s software stack to scale. High growth technology businesses need to be prepared to make significant investments in product development to continue gaining market traction. This means a willingness by CFOs to move further out on the risk curve, recommending the extent of these investments, taken in the context of the company’s life cycle, maturity, addressable market, and liquidity requirements. Not adequately funding these efforts could restrain growth and create barriers to a fast-growing company achieving the critical mass required to hit a target business model at scale.

Partner with the Business, especially the Go-To-Market side

Even when product/market fit is established, hypergrowth won’t occur without a sound go-to-market strategy and aggressive actions to gain market share. Finance leadership should therefore look to build a strong partnership with sales leaders and strategize around how the finance team can add value to furthering revenue objectives. These conversations should yield decisions around efficiently scaling the footprint of the sales organization while entering new markets and the economics behind channel partnerships. In SAAS businesses, key focus areas include for example; ARR, MRR, months to recover CAC, net and gross dollar-based retention rates, upsell trends, churn and instrumenting all of your metrics for monitoring on a daily basis. Other areas to explore are whether outsourcing customer service functions should be considered to improve velocity and customer satisfaction. A sales compensation structure that properly incentivizes over performance and attracts the best talent is key, as well as insuring the right control framework is in place to properly vet deals, while avoiding bureaucratic gridlock.

While there is certainly still an element of Finance’s old-school command and control role, modern finance leaders should always be looking for ways to step outside the confines of internal controls and policy prescriptions to leverage their analytical skills to support sound decision making. I know my team has succeeded in this regard when the functional team leaders across the business view their FP&A partner more a part of their team than the finance org. In fact, although it may seem trivial, I encourage FP&A business partners to sit with the teams they support. This creates a culture of constant interaction and collaboration, especially in open office environments. In hypergrowth, decisions are being made daily in real-time, and finance leaders can add tremendous value cross-functionally by providing clear monetary guardrails to ensure both sustainable top-line revenue growth and a path to profitability are prioritized.

Drive Strategic Business Planning

Once a finance leader begins to develop a more holistic view of a business then they are in a position to more fully participate with the CEO and the rest of the management team in aggressively scaling a company. It is surprising to me how many high growth companies with substantial scale ($100M+) do not have a developed planning process. In fact, the CFO is in an ideal position to drive the bigger picture of hypergrowth strategy and the financial implications. This requires a shift away from just prioritizing short-term gains to insure there is a proper balanced with long-term value creation.

A well-designed planning process starts with the development of a Long-Term Strategic Plan, which sets the foundation for investment decisions that drive the product road map, global expansion and investments across every functional area, leading ultimately to next year’s operating plan. Whether the planning horizon selected is 3 years (my preference) or up to 5 years, the Strategic Plan sets the Longer-Term Strategic Goals and Key Results, and the resulting Financial Model Targets by year. A longer-term view is important because it provides context for investments made and decisions/trade-offs in the current year – that is, without a longer-term view, a short-term focus may lead to poor choices.

Communicating the results of this process to employees is just as important as the process itself. Employees need to understand where a company is heading, the priorities, key objectives over both the next several years and those tied to next year’s operating plan that everyone will be held accountable to deliver on. This is normally augmented with a Quarterly Review Process to assess progress against objectives, which is particularly impactful in hypergrowth companies as they iterate so rapidly. The necessary real-time course-corrections required to achieve escape velocity for technology startups places pressure on the CFO to manage a constantly evolving view of the future.

Invest in People

Scaling in virtually all cases means hypergrowth companies are growing headcount very rapidly. After operating in hypergrowth environments in which headcount grew from a few hundred to a few thousand employees in 24 months, I saw firsthand the many challenges across multiple dimensions this creates. Others have written extensively on effectively scaling headcount in hypergrowth environments. Claire Hughes Johnson, the COO of Stripe wrote a great article on how Stripe met these challenges, which I highly recommend To Grow Faster, Hit Pause. However, there are a few important points that CFO’s should consider.

First, the CHRO is a key relationship for every CFO, since people-related costs typically represent the most significant cost element in a technology business. Second, the CFO needs to weigh in on a plan for a cohesive organizational structure and strong leadership for functional groups, starting at the C suite level, cascading down through the director and manager level, in order to absorb and integrate new employees efficiently. It is not unusual to find employees thrust into positions managing big teams with little to no management experience. Finance leaders therefore need to recognize that resources are not only required for talent acquisition, but organizational development. It is easy to cut spending in this area in the capital allocation process. However, dismissing the need for these investments results in hidden costs by way of poor management, which can be significant, since issues get magnified when growing at high velocity. Third, preservation of the company culture is one of the largest challenges when adding people quickly, since new employees import values from their previous experience. Your culture therefore can be easily diluted without a deliberate effort to define your operating principles, and incorporating those principles into the hiring, onboarding and performance review processes. Getting this right directly impacts the operating performance of a hypergrowth company and its ability to hit financial targets and other milestones outlined in the company’s business plan.

Focus on scaling IT Systems and Processes

Proper scaling of a company’s IT infrastructure and business systems is of high relevance for finance leadership. Upgrading a company’s business systems, a non-trivial task, is very typical in a rapidly growing business. Smaller companies do not have the scale to justify these investments. IT plays a pivotal role in ensuring that management is receiving accurate data through business intelligence systems and that there is one source of truth. There is no worse feeling than flying blind when you are in hypergrowth mode. Inaccurate data prevents management from understanding the changing dynamics in a business, which can lead to significant issues not being surfaced and poor decision making. This in turn can lead to restrictions on growth and financial exposure to lower performance. These investments can be large and therefore they represent another area in the capital allocation process that finance leadership should weigh in on.

Operate Like a Public Company, even if you are not sure of your exit strategy

While many executives may complain about the rigors that get imposed on a business operating as a public company, these rigors allow management to more effectively run a business and the CFO must lead the charge. A strong internal control framework, and documented business processes are needed regardless of whether a company is planning an IPO or not, and are especially important if a company is in hypergrowth mode. In fact, when I look to build my teams, I always lean toward candidates who have operated in larger public companies, and have demonstrated an ability to think outside the box, because they have already learned the many disciplines required and have overcome challenges in creative ways. When in hypergrowth mode, I over-hire, projecting where I think the company will be 3 or 4 years down the road. Having the benefit of operating at larger scale results in being able to articulate a clearer roadmap for how to get there. With high growth companies, there is no time for learning on the job.

Operating like a public company also extends to other areas of corporate governance, such as the audit committee. Chris Paisley, the former CFO of 3Com and one of the more prominent audit committee chairs in Silicon Valley (including my audit chair at Fitbit), shared with me that as a CFO he viewed the audit committee as his board of directors. Frequent interaction between the CFO and the audit committee, especially the audit chair, results in strong governance and avoids surprises. Even though I am the audit chair of a public company, I always look to bounce ideas and ask for advice from my audit chair where I am the CFO. We are all constantly learning, and many audit chairs, especially those who sit on multiple boards, have a wealth of experience from other businesses that could potentially be applied to help a sitting CFO deal with challenges. When a company is moving at breakneck speed, executives need all the help and advice they can get, and the CFO is no exception, regardless of experience level.

Recognize hypergrowth and optimization can be conflicting goals

It can be very challenging to grow quickly and optimize at the same time. This can be frustrating for finance leaders, since optimization and efficiency are typically in our blood. When a business is already at a reasonable level of scale ($100M+) and growing at 50-100% a year, there are times that management needs to deliberately slow down and take a step back. Executives need to understand how the company is set up to scale a function or enter a particular market well before the sheer momentum of the business drags everyone along. The CFO can play a pivotal role by providing this insight along the way. Much of this relates to how ingrained the company’s operating principles are with the scaling of the organization. Are decisions being made consistent with those principles and are managers being thoughtful about consuming resources? While mid-course corrections are typically needed to tune an organization along the way that is growing very quickly, the CFO should recognize that trade-offs must be made, and that additional optimization may become a future focus when the business reaches more maturity.

Own the Path to Profitability

An enterprise is valued based on the discounted value of future cash flows. Taking ownership in the path to profitability falls on the shoulders of finance leadership. While it is expected that hypergrowth companies need to make large investments and will generate losses on the way towards a target business model, Wall Street has recently provided a wake-up call. Companies generating enormous losses that recently went public either entered the public markets at lower than expected valuations, or in some cases failed to do so at all. This is a signal to Silicon Valley companies that more financial discipline is needed and that the public markets will not blindly fund large losses without a proven business model featuring strong unit economics, and a clear path to sustainable profitability. Investors are particularly focused on unit economics and the resulting gross margin. A rapidly scaling top line is great, but strong gross margins reflect the strength of the customer value proposition and are highly correlated to valuation metrics. There is no level of growth that can overcome inherently poor unit economics. I have never believed that “growth at all costs” is justified, and in fact fast-growth companies that enter the public markets with either marginal losses or already generating some profit are handsomely rewarded.

When we took Fitbit public in 2015, we were marginally profitable and in our first full year as a public company our Adjusted EBITDA was just shy of $400 million. That was the result of a deliberate focus on scaling the bottom line along with the top line. In fact, Fitbit grew revenues to $1 billion on $22 million of invested capital, unprecedented for a consumer tech product company. Establishing that discipline early on creates a company culture that acknowledges financial performance should be a core focus for a business. That said, supporting the right investments is critical because building for the long term is the path to generating significant shareholder value. Installing business processes to properly review and scrutinize discretionary spending and investment sends a message across a business that management takes this responsibility seriously and will not be frivolous with financial resources. In all my CFO roles at late stage companies that were scaling, I personally reviewed in a weekly meeting discretionary spending above a certain level, which changed over time as the company grew. This gave me and my team great insight into company spending patterns and allowed us to ingrain a discipline around spending and investment decisions as we grew our Opex envelope.

In Summary

While in this article I have covered the salient points that in my experience enable CFOs to step up and play a vital role in scaling a hypergrowth business, there are a litany of details below the surface in the actual execution. I have been privileged to work alongside phenomenal teams, and have learned many lessons along the way that allowed me to operate more effectively in the future, and I continue to learn. High velocity in a company can be both exhausting and exhilarating at the same time. Hypergrowth technology companies are disrupting industries around the world and changing the way we live. More than ever, CFOs can play a leading role in helping these companies achieve their potential.

Bill Zerella is an accomplished financial executive and business partner with over 30 years of results-oriented leadership and broad-based experience in both public and privately held, venture-backed software and hardware global technology businesses.

Bill is highly experienced in building teams and scaling hypergrowth businesses through an IPO and beyond, has raised over $2.5 Billion in capital and been part of teams that have created billions in shareholder value.

I had the good fortune of being raised in a family that put a high value on educating the whole person. What I mean by that is that academics were really important, but more important was instilling a sense of curiosity about all things surrounding us: culture, spirituality, community, art, knowledge, and athletics—not as a viewer but as a participant. My parents were not focused on getting their nine children (of which I was number nine) into the most prestigious colleges, they were focused on educating the whole person and getting us ready for the excitement and vagaries of the world. To this end, my dad pulled off a great barter trade with the Woodside Priory School; he taught first period algebra in turn for our attendance at the Benedictine College Prep School. The school’s philosophy dove-tailed perfectly with that of my parents. We received an exceptional gift of a great education and a true head start in life.

Lessons learned from the Benedictine Monks

The school was founded by Benedictine monks who had emigrated from Hungry to escape the communist takeover of that country following WWII. We learned a great deal about all world religions at the Priory. Included in our education was some exposure to The Rule of St. Benedict, which in fact is sort of a playbook on how 8th century monks should go about their lives. St. Benedict was the founding father of the Benedictine order and had numerous rules for his followers, many of which still have practical applications today. One has stuck with me in business and life: To always “listen with the ear of the heart.” There are complete books written about what this means, but in my world, I apply it to serving my clients and candidates in the best possible way.

Non-listening Consultant Gets Shown the Door

I met with a new CEO client a couple of months ago who had recently engaged a retained search for a CIO. I asked him what he liked and disliked about that process. I was somewhat shocked by what he said. He told me the search consultant asked a lot of good questions of him, but the search consultant seemingly did not listen to any of the answers and direction given. For example, the CEO wanted the consultant to find a fresh slate of candidates for his company needs, not just re-use his existing candidates who were not hired in his last search. But this was exactly what the consultant did. Huh? The CEO decided to part ways with the consultant.

Listening with the Ear of the Heart

As a CFO and Audit Committee Member search consultant, I would argue that listening effectively to our clients and candidates is the most important thing a search consultant does. Second only to asking incisive questions so we can gather the truth and make excellent lasting matches. This all starts in my mind with “listening with the ear of the Heart.” I do not mean this in a religious way, rather just opening yourself up to the person speaking, having both empathy and sometimes sympathy for their words and experiences. It is not just taking notes and deciding what they really mean based on assumption. It is not just hearing and writing, it is looking for the meaning behind the words they choose. It is feeding back their words to make sure you really understand what they said.

During our discovery interviews with clients when kicking off a Board recruitment process or CFO search process we receive a lot of information. We circle back with the CEO after meeting her team or get back with the Chairman after meeting board members to make sure we listened deeply and understand clearly what the client needs and wants. Of course, we also chime in and offer guidance where there may be confusion or differences of opinion.

The CEO client I referred to earlier has an affinity for vocabulary and etymology, which I share. We got into some pretty funny discussions about words, where they come from, and the importance of choosing words thoughtfully when explaining ourselves and our companies. In writing the CFO specification for this client I was very careful to use many of the exact words he used in describing what he wanted in a CFO and how he characterized his company culture. This is listening with the ear of the Heart—listening and understanding the words and applying them to make a match between the management’s intentions and the intentions of prospective executive hire.

Making Matches that Last

Some of my recruiting friends say what I do must get boring, just placing CFOs and Audit Committee members. Au contraire. No two CEOs are the same, no two CFOs are the same. It is all in the subtlety of language, both verbal and non-verbal. The only way to make a good match is to really, really listen. Then take those words to heart and re-use them not only in writing a specification but in interviewing and presenting. This will result in a match that will last. I would argue that the only way to do that is to listen with the ear of the heart. Thanks Dad, thanks Priory, and thanks St. Benedict; our placed CFOs have an average tenure over five years! Now that is making matches that last.

If you are seeking a financially minded Board Member or CFO who listens deeply and delivers lasting results, thanks for reaching out to me at moc.srentrapdlonra@evad.