The CFO’s Role in Scaling a Hypergrowth Technology Company

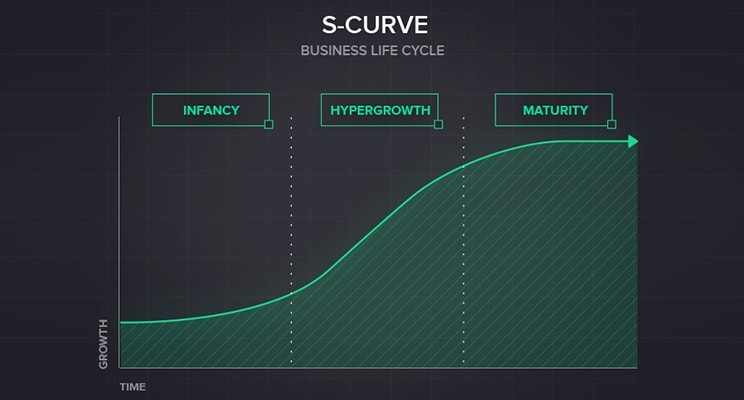

CFOs play a vital role in the scaling of any business. Young technology businesses however pose their own unique challenges. Coupling those challenges with hypergrowth results in extraordinary demands on the management of a company. First coined by Alexander V. Izosimov in the Harvard Business Review in 2008 Managing Hypergrowth, “hypergrowth” refers to the steep part of the S-curve, where industries and firms grow at an explosive pace. Hypergrowth businesses rapidly expand with compound annual growth rates (CAGR) that can exceed 50%, and in some cases even above 100%. This means hypergrowth companies need to insure they have the right people and systems in place to support such high velocity, so they do not go off the rails.

At the same time, the CFO role has extended its reach into every corner of a company. In most companies the CFO, more than any other executive, is a true business partner to the CEO. Therefore, as hypergrowth companies work at a frenetic pace to meet the many challenges, chances are the CFO will play a major role. So how can CFOs effectively expand their influence and add value in these hypergrowth technology focused environments?

Think Strategically

In many companies, CFOs are being called on to play a bigger role in setting strategy. The CFO’s traditional role as steward, operator and catalyst now includes a large dose of strategy in addition to the more traditional role that focuses on core competencies such as accounting, tax, financial reporting, internal controls, budgeting and forecasting, investor relations, fraud awareness and prevention, risk management and corporate governance. This was certainly the case in some of my previous roles as CFO where I was responsible for the Strategic Planning function. In order to expand their skill set, CFOs must therefore move up the value chain from being stewards of compliance to becoming strategic executives.

Developing a strategic view requires gaining a holistic understanding of a business and starts with understanding the product value proposition.

- Why are customers buying the company’s products?

- Does the company have a repeatable solution that is solving a clear pain point?

- Are the unit economics self-evident, sustainable, and based on relevant metrics?

- Where is the company in the product adoption lifecycle?

- How does the company aggressively extend its product relevance to rapidly gain share?

- How can strategic M&A further accelerate share penetration by filling in product gaps?

The most effective CFOs can serve up cogent, actionable answers to these critical questions. While this does not mean the CFO needs to be an engineer or a technology guru, it does mean the CFO should understand what is driving top line revenue, the core of any hypergrowth business. Even if there is a separate strategy function reporting into the CEO, which is not uncommon, the CFO should engage with the strategy team and understand the competitive dynamics and clear choice the company has made to either disrupt an industry with entrenched incumbents or pioneer a new market. Developing this understanding is crucial for finance leadership to play an active role in making decisions on capital allocation.

This includes a more detailed roadmap for the specific areas where the company plans to innovate and the related cost drivers. For example, with software businesses, understanding the extent of “Tech Debt” may sound at first like it is beyond the scope of finance leaders. Tech Debt is cholesterol in the arteries of startup growth: the overhead associated with previous shortcuts being taken in software development which increasingly impede future scalability efforts. This is important for the CFO to consider because it directly impacts future costs which need to be accounted for in the financial model to allow a company’s software stack to scale. High growth technology businesses need to be prepared to make significant investments in product development to continue gaining market traction. This means a willingness by CFOs to move further out on the risk curve, recommending the extent of these investments, taken in the context of the company’s life cycle, maturity, addressable market, and liquidity requirements. Not adequately funding these efforts could restrain growth and create barriers to a fast-growing company achieving the critical mass required to hit a target business model at scale.

Partner with the Business, especially the Go-To-Market side

Even when product/market fit is established, hypergrowth won’t occur without a sound go-to-market strategy and aggressive actions to gain market share. Finance leadership should therefore look to build a strong partnership with sales leaders and strategize around how the finance team can add value to furthering revenue objectives. These conversations should yield decisions around efficiently scaling the footprint of the sales organization while entering new markets and the economics behind channel partnerships. In SAAS businesses, key focus areas include for example; ARR, MRR, months to recover CAC, net and gross dollar-based retention rates, upsell trends, churn and instrumenting all of your metrics for monitoring on a daily basis. Other areas to explore are whether outsourcing customer service functions should be considered to improve velocity and customer satisfaction. A sales compensation structure that properly incentivizes over performance and attracts the best talent is key, as well as insuring the right control framework is in place to properly vet deals, while avoiding bureaucratic gridlock.

While there is certainly still an element of Finance’s old-school command and control role, modern finance leaders should always be looking for ways to step outside the confines of internal controls and policy prescriptions to leverage their analytical skills to support sound decision making. I know my team has succeeded in this regard when the functional team leaders across the business view their FP&A partner more a part of their team than the finance org. In fact, although it may seem trivial, I encourage FP&A business partners to sit with the teams they support. This creates a culture of constant interaction and collaboration, especially in open office environments. In hypergrowth, decisions are being made daily in real-time, and finance leaders can add tremendous value cross-functionally by providing clear monetary guardrails to ensure both sustainable top-line revenue growth and a path to profitability are prioritized.

Drive Strategic Business Planning

Once a finance leader begins to develop a more holistic view of a business then they are in a position to more fully participate with the CEO and the rest of the management team in aggressively scaling a company. It is surprising to me how many high growth companies with substantial scale ($100M+) do not have a developed planning process. In fact, the CFO is in an ideal position to drive the bigger picture of hypergrowth strategy and the financial implications. This requires a shift away from just prioritizing short-term gains to insure there is a proper balanced with long-term value creation.

A well-designed planning process starts with the development of a Long-Term Strategic Plan, which sets the foundation for investment decisions that drive the product road map, global expansion and investments across every functional area, leading ultimately to next year’s operating plan. Whether the planning horizon selected is 3 years (my preference) or up to 5 years, the Strategic Plan sets the Longer-Term Strategic Goals and Key Results, and the resulting Financial Model Targets by year. A longer-term view is important because it provides context for investments made and decisions/trade-offs in the current year – that is, without a longer-term view, a short-term focus may lead to poor choices.

Communicating the results of this process to employees is just as important as the process itself. Employees need to understand where a company is heading, the priorities, key objectives over both the next several years and those tied to next year’s operating plan that everyone will be held accountable to deliver on. This is normally augmented with a Quarterly Review Process to assess progress against objectives, which is particularly impactful in hypergrowth companies as they iterate so rapidly. The necessary real-time course-corrections required to achieve escape velocity for technology startups places pressure on the CFO to manage a constantly evolving view of the future.

Invest in People

Scaling in virtually all cases means hypergrowth companies are growing headcount very rapidly. After operating in hypergrowth environments in which headcount grew from a few hundred to a few thousand employees in 24 months, I saw firsthand the many challenges across multiple dimensions this creates. Others have written extensively on effectively scaling headcount in hypergrowth environments. Claire Hughes Johnson, the COO of Stripe wrote a great article on how Stripe met these challenges, which I highly recommend To Grow Faster, Hit Pause. However, there are a few important points that CFO’s should consider.

First, the CHRO is a key relationship for every CFO, since people-related costs typically represent the most significant cost element in a technology business. Second, the CFO needs to weigh in on a plan for a cohesive organizational structure and strong leadership for functional groups, starting at the C suite level, cascading down through the director and manager level, in order to absorb and integrate new employees efficiently. It is not unusual to find employees thrust into positions managing big teams with little to no management experience. Finance leaders therefore need to recognize that resources are not only required for talent acquisition, but organizational development. It is easy to cut spending in this area in the capital allocation process. However, dismissing the need for these investments results in hidden costs by way of poor management, which can be significant, since issues get magnified when growing at high velocity. Third, preservation of the company culture is one of the largest challenges when adding people quickly, since new employees import values from their previous experience. Your culture therefore can be easily diluted without a deliberate effort to define your operating principles, and incorporating those principles into the hiring, onboarding and performance review processes. Getting this right directly impacts the operating performance of a hypergrowth company and its ability to hit financial targets and other milestones outlined in the company’s business plan.

Focus on scaling IT Systems and Processes

Proper scaling of a company’s IT infrastructure and business systems is of high relevance for finance leadership. Upgrading a company’s business systems, a non-trivial task, is very typical in a rapidly growing business. Smaller companies do not have the scale to justify these investments. IT plays a pivotal role in ensuring that management is receiving accurate data through business intelligence systems and that there is one source of truth. There is no worse feeling than flying blind when you are in hypergrowth mode. Inaccurate data prevents management from understanding the changing dynamics in a business, which can lead to significant issues not being surfaced and poor decision making. This in turn can lead to restrictions on growth and financial exposure to lower performance. These investments can be large and therefore they represent another area in the capital allocation process that finance leadership should weigh in on.

Operate Like a Public Company, even if you are not sure of your exit strategy

While many executives may complain about the rigors that get imposed on a business operating as a public company, these rigors allow management to more effectively run a business and the CFO must lead the charge. A strong internal control framework, and documented business processes are needed regardless of whether a company is planning an IPO or not, and are especially important if a company is in hypergrowth mode. In fact, when I look to build my teams, I always lean toward candidates who have operated in larger public companies, and have demonstrated an ability to think outside the box, because they have already learned the many disciplines required and have overcome challenges in creative ways. When in hypergrowth mode, I over-hire, projecting where I think the company will be 3 or 4 years down the road. Having the benefit of operating at larger scale results in being able to articulate a clearer roadmap for how to get there. With high growth companies, there is no time for learning on the job.

Operating like a public company also extends to other areas of corporate governance, such as the audit committee. Chris Paisley, the former CFO of 3Com and one of the more prominent audit committee chairs in Silicon Valley (including my audit chair at Fitbit), shared with me that as a CFO he viewed the audit committee as his board of directors. Frequent interaction between the CFO and the audit committee, especially the audit chair, results in strong governance and avoids surprises. Even though I am the audit chair of a public company, I always look to bounce ideas and ask for advice from my audit chair where I am the CFO. We are all constantly learning, and many audit chairs, especially those who sit on multiple boards, have a wealth of experience from other businesses that could potentially be applied to help a sitting CFO deal with challenges. When a company is moving at breakneck speed, executives need all the help and advice they can get, and the CFO is no exception, regardless of experience level.

Recognize hypergrowth and optimization can be conflicting goals

It can be very challenging to grow quickly and optimize at the same time. This can be frustrating for finance leaders, since optimization and efficiency are typically in our blood. When a business is already at a reasonable level of scale ($100M+) and growing at 50-100% a year, there are times that management needs to deliberately slow down and take a step back. Executives need to understand how the company is set up to scale a function or enter a particular market well before the sheer momentum of the business drags everyone along. The CFO can play a pivotal role by providing this insight along the way. Much of this relates to how ingrained the company’s operating principles are with the scaling of the organization. Are decisions being made consistent with those principles and are managers being thoughtful about consuming resources? While mid-course corrections are typically needed to tune an organization along the way that is growing very quickly, the CFO should recognize that trade-offs must be made, and that additional optimization may become a future focus when the business reaches more maturity.

Own the Path to Profitability

An enterprise is valued based on the discounted value of future cash flows. Taking ownership in the path to profitability falls on the shoulders of finance leadership. While it is expected that hypergrowth companies need to make large investments and will generate losses on the way towards a target business model, Wall Street has recently provided a wake-up call. Companies generating enormous losses that recently went public either entered the public markets at lower than expected valuations, or in some cases failed to do so at all. This is a signal to Silicon Valley companies that more financial discipline is needed and that the public markets will not blindly fund large losses without a proven business model featuring strong unit economics, and a clear path to sustainable profitability. Investors are particularly focused on unit economics and the resulting gross margin. A rapidly scaling top line is great, but strong gross margins reflect the strength of the customer value proposition and are highly correlated to valuation metrics. There is no level of growth that can overcome inherently poor unit economics. I have never believed that “growth at all costs” is justified, and in fact fast-growth companies that enter the public markets with either marginal losses or already generating some profit are handsomely rewarded.

When we took Fitbit public in 2015, we were marginally profitable and in our first full year as a public company our Adjusted EBITDA was just shy of $400 million. That was the result of a deliberate focus on scaling the bottom line along with the top line. In fact, Fitbit grew revenues to $1 billion on $22 million of invested capital, unprecedented for a consumer tech product company. Establishing that discipline early on creates a company culture that acknowledges financial performance should be a core focus for a business. That said, supporting the right investments is critical because building for the long term is the path to generating significant shareholder value. Installing business processes to properly review and scrutinize discretionary spending and investment sends a message across a business that management takes this responsibility seriously and will not be frivolous with financial resources. In all my CFO roles at late stage companies that were scaling, I personally reviewed in a weekly meeting discretionary spending above a certain level, which changed over time as the company grew. This gave me and my team great insight into company spending patterns and allowed us to ingrain a discipline around spending and investment decisions as we grew our Opex envelope.

In Summary

While in this article I have covered the salient points that in my experience enable CFOs to step up and play a vital role in scaling a hypergrowth business, there are a litany of details below the surface in the actual execution. I have been privileged to work alongside phenomenal teams, and have learned many lessons along the way that allowed me to operate more effectively in the future, and I continue to learn. High velocity in a company can be both exhausting and exhilarating at the same time. Hypergrowth technology companies are disrupting industries around the world and changing the way we live. More than ever, CFOs can play a leading role in helping these companies achieve their potential.

Bill Zerella is an accomplished financial executive and business partner with over 30 years of results-oriented leadership and broad-based experience in both public and privately held, venture-backed software and hardware global technology businesses.

Bill Zerella is an accomplished financial executive and business partner with over 30 years of results-oriented leadership and broad-based experience in both public and privately held, venture-backed software and hardware global technology businesses.

Bill is highly experienced in building teams and scaling hypergrowth businesses through an IPO and beyond, has raised over $2.5 Billion in capital and been part of teams that have created billions in shareholder value.